黄仁勋亮相COMPUTEX 2026,聚焦AI生态系最新进展 · Jensen Huang Takes the Stage at COMPUTEX 2026 to Unveil Latest AI Innovations

你好,希望你今天一切都好。

Hello, hope you’re having a great day.

台北Computex 2026将于6月2日至5日举行。NVIDIA创始人兼CEO黄仁勋将于台湾时间6月1日(周一)上午11点(美西时间5月31日晚8点)在台北流行音乐中心发表主题演讲,现场直播同步开启,重播可于nvidia.com/zh-tw/gtc/taipei/keynote/观看。本次演讲将公布NVIDIA最新AI技术进展,聚焦运算、物理AI与代理系统三大方向,并展示其”五层蛋糕”架构——从能源基础到上层应用,呈现整个生态系如何协同扩展以支撑下一波创新浪潮。GTC Taipei将于6月2至4日在台北国际会议中心举办,涵盖主题演讲、技术论坛、现场展示及生态系交流活动,重点聚焦物理AI、AI工厂、代理系统与推论四大领域。GTC不仅是一场技术大会,更是AI生态系的全球平台,连接开发者、研究人员与企业领袖,让创意从概念走向实际部署,合作伙伴关系则持续推动下一波创新扩展。此前,NVIDIA与Palantir宣布建立自主AI合作伙伴关系,联合开发预装八颗Blackwell Ultra GPU及NVIDIA网络设备的系统,供各国政府直接部署至安全设施;阿联酋企业Aleria亦已订购8,640颗Blackwell Ultra芯片,并计划将采购规模扩大近一倍。过去两年AI算力的核心买家是超大规模云厂商,如今政府客户正在加速入场,或将成为下一阶段AI采购的重要驱动力。

Computex 2026 runs from June 2 to 5 in Taipei. NVIDIA founder and CEO Jensen Huang will deliver a keynote at the Taipei Music Center on Monday, June 1 at 11 AM Taiwan Time (8 PM PT on May 31), with a live stream available and replay accessible at nvidia.com/zh-tw/gtc/taipei/keynote/. The keynote will unveil NVIDIA’s latest AI advancements, centered on three pillars: computing, physical AI, and agentic systems. It will also showcase the company’s “Five-Layer Cake” architecture — spanning from energy infrastructure to application layers — illustrating how the broader ecosystem is scaling to support the next wave of innovation. GTC Taipei follows from June 2 to 4 at the Taipei International Convention Center, featuring keynotes, technical sessions, live demonstrations, and ecosystem networking events, with a focus on physical AI, AI factories, agentic systems, and inference. GTC is more than a conference — it is a global platform for the AI ecosystem, bringing together developers, researchers, and enterprise leaders to take ideas from concept to deployment, with partnerships driving the expansion of the next innovation wave. Ahead of the event, NVIDIA and Palantir announced an autonomous AI partnership to co-develop systems pre-loaded with eight Blackwell Ultra GPUs and NVIDIA networking gear for direct government deployment in secure facilities; UAE-based Aleria also placed an order for 8,640 Blackwell Ultra chips with plans to nearly double that figure. Hyperscalers have been the dominant AI compute buyers over the past two years — governments are now emerging as a fast-growing customer segment and may become a significant driver of AI procurement in the next phase.

全球首台NVIDIA Vera Rubin VR200 NVL72机柜由CoreWeave与戴尔联合完成交付,并一次性通过L11全机柜级硬件诊断测试。这不仅仅是原型机的亮相,而是NVIDIA下一代AI算力平台从路线图走向现实的关键里程碑。单台机柜集成72颗Rubin GPU与36颗Vera CPU,采用全NVLink 6互联、HBM4内存与液冷设计,推理性能直指3.6 exaFLOPS量级。相比Blackwell,单GPU算力提升约3.5倍,内存带宽提升约2.8倍。此次交付顺利通过测试,意味着HBM4、先进封装、液冷系统等核心供应链环节均未出现重大瓶颈,早期Blackwell曾遭遇的内存与散热问题在Rubin这一代并未重演。这一结果提前锁定了2026年下半年的AI算力供应确定性,也进一步打消了市场对Rubin延期的顾虑。随着训练与推理成本曲线持续下行,万亿参数模型的迭代周期将进一步压缩,多步推理与外部存储等能力也将真正落地成形。

The world’s first NVIDIA Vera Rubin VR200 NVL72 cabinet has been jointly delivered by CoreWeave and Dell, passing the L11 full-cabinet hardware diagnostic test in a single attempt. This is more than a prototype milestone — it marks the transition of NVIDIA’s next-generation AI compute platform from roadmap to reality. Each cabinet integrates 72 Rubin GPUs and 36 Vera CPUs, featuring full NVLink 6 interconnects, HBM4 memory, and liquid cooling, with inference performance targeting the 3.6 exaFLOPS range. Compared to Blackwell, single-GPU compute improves by approximately 3.5x and memory bandwidth by around 2.8x. The clean pass-through indicates no major bottlenecks across critical supply chain components including HBM4, advanced packaging, and liquid cooling — issues that had affected early Blackwell generations were not repeated here. This effectively locks in AI compute supply certainty for the second half of 2026 while dispelling market concerns over potential Rubin delays. As training and inference cost curves continue to decline, iteration cycles for trillion-parameter models will compress further, and capabilities such as multi-step reasoning and external memory will move from concept to reality.

从供应链传导来看,Rubin每台机柜的HBM4用量约达20.7TB,叠加NVLink 6交换机、ConnectX-9、BlueField-4等新型芯片,对整条产业链形成端到端的强劲拉动。SK海力士、三星、美光三大存储厂商的HBM4价格与出货量预计将进一步上行;台积电先进制程与CoWoS先进封装订单有望持续增长;液冷、电源模块、互联组件等基础设施供应商将直接受益,800V高压直流配电亦被视为新的关注热点。Dell与CoreWeave再度扮演”全球首发”先锋角色,AI服务器订单与云服务护城河大幅提升,CRWV作为NVIDIA核心合作伙伴的地位也得到进一步验证。

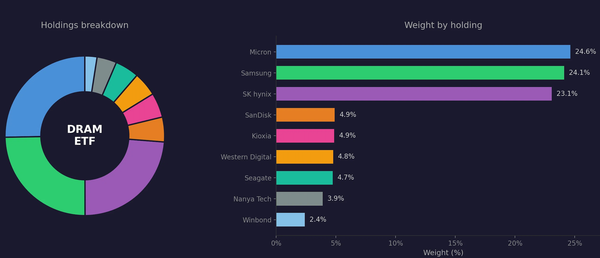

From a supply chain perspective, each Rubin cabinet consumes approximately 20.7TB of HBM4, and combined with new components such as NVLink 6 switches, ConnectX-9, and BlueField-4, the end-to-end pull-through across the supply chain is substantial. HBM4 pricing and shipment volumes for the three major memory players — SK Hynix, Samsung, and Micron — are expected to trend higher. TSMC’s advanced process and CoWoS advanced packaging orders are likely to continue surging. Infrastructure providers in liquid cooling, power modules, and interconnect components stand to benefit directly, with 800V high-voltage DC power distribution emerging as a new area of focus. Dell and CoreWeave once again claimed the “global first” position, significantly elevating their AI server order pipelines and cloud service moats, while CRWV’s status as NVIDIA’s favored partner received further validation.

宏观层面,本周有两项数据值得重点关注。5月非农就业报告将于周五上午8:30(美东时间)公布。4月数据显示新增就业11.5万人,远超经济学家预期的5.5万人,失业率维持在4.3%,工资同比增长3.6%,劳动力市场呈现温和降温而非剧烈波动的态势。新任美联储主席Kevin Warsh将于6月16至17日主持首次议息会议,市场目前几乎未定价2026年剩余时间的降息预期,因此周五数据将是Warsh就任前最后一份重要劳动力市场参考。此外,ISM制造业指数将于周一上午10点公布,4月读数为52.7;ISM服务业指数将于周三上午10点公布,4月读数为53.6,已连续22个月保持扩张。目前值得关注的结构性分歧是:制造业增速有所放缓,而服务业仍在独力支撑经济扩张。当一台引擎减速而另一台独力运转时,双引擎是否能够同步重启,是判断经济韧性的关键所在。

On the macro front, two data points deserve close attention this week. The May non-farm payrolls report is due Friday at 8:30 AM ET. April’s reading came in at 115,000 new jobs, well above the economist consensus of 55,000, with the unemployment rate holding at 4.3% and wages up 3.6% year-over-year — a picture of gradual cooling rather than sharp deterioration. New Fed Chair Kevin Warsh chairs his first policy meeting on June 16–17, with markets currently pricing in almost no rate cuts for the remainder of 2026, making Friday’s release the final significant labor market data point before Warsh takes the chair. The ISM Manufacturing Index is due Monday at 10 AM, with April at 52.7; the ISM Services Index follows Wednesday at 10 AM, with April at 53.6 and now 22 consecutive months of expansion. The structural divergence worth watching: manufacturing momentum is fading while services continues to carry the expansion alone. Whether the second engine can reignite alongside the first is the key test of economic resilience ahead.