ASTS 突破基本目标价及乐观目标价 · 后市策略 Breaks Base and Optimistic Price Targets · Strategy Update

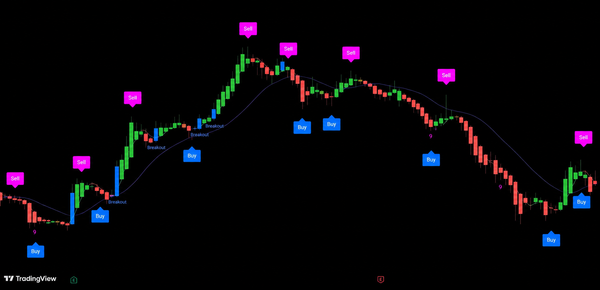

$ASTS 升破基本目标价 110 及乐观目标价 130,今日再创历史新高。

$ASTS has broken through the base target of USD 110 and the optimistic target of USD 130, reaching a new all-time high today.

恭喜约十几天前在低位重新建仓的会员,短短时间内斩获约 90% 的升幅。所有操作记录均已公开于会员平台,供会员随时核对。

Congratulations to members who rebuilt positions at lower levels roughly two weeks ago, achieving a gain of approximately 90% in a short period. All trade records have been published on the member platform for full transparency.

5月12日,$ASTS 财报发布后股价单日急跌逾10%。市场上大量KOL开始发布针对这间公司的负面评价,看空声音一时甚嚣尘上。团队在当天即时发布分析,明确表态:下跌不改变长期论点,这是机构在低位持续积累的过程,而非逻辑破裂的信号。

On May 12, $ASTS fell sharply by more than 10% following its earnings release. A wave of KOLs began publishing negative commentary on the company, with bearish voices dominating the conversation. The team published an analysis the same day, stating clearly: the decline did not change the long-term thesis. This was a process of institutional accumulation at lower levels — not a breakdown in the investment case.

十几天后,股价不仅完全收复失地,更接连突破团队此前设定的基本目标价 110 美元与乐观目标价 130 美元,今日再度刷新历史最高价。市场就是如此戏剧性——最悲观的时刻,往往正是最好的机会所在。

Just over two weeks later, the stock had not only fully recovered — it broke through the team’s previously set base target of USD 110 and optimistic target of USD 130 in succession, reaching a new all-time high today. The market has a way of being dramatic — the most pessimistic moments are often where the best opportunities reside.

近期走势已越来越不像一只普通的高波动太空概念股。过去连续两天,市场出现异常庞大的 MOC(收盘集合竞价)订单,且成交位置恰好集中在接近历史新高附近。今日收盘竞拍中可观察到多个高度规则的大宗成交块:250K × 4、340K、313K、154K,估计逾 180 万股,按收盘价折算约超过 2.4 亿美元。这种高度统一的成交节奏,并不像随机散户行为,更像是有计划的大资金在固定时间持续参与。

Recent price action is increasingly unlike a typical high-volatility space concept stock. Over the past two consecutive days, unusually large Market-On-Close orders have appeared, concentrated precisely near all-time high levels. Today’s closing auction revealed multiple highly uniform block trades: 250K × 4, 340K, 313K, and 154K — estimated at over 1.8 million shares, translating to approximately USD 240 million or more at the closing price. This level of order uniformity does not resemble random retail activity; it more closely resembles structured institutional participation at pre-planned intervals.

市场目前最大的争议在于:这些成交究竟是机构在积累筹码,还是空头在被迫回补?空头回补在理论上成立——当高空头、高波动股票持续逼近历史高位,持仓过夜的压力会迅速累积。然而,仔细分析成交结构后,这里有一点不像典型的 short covering。空头通常会选择盘中逐步回补以降低市场冲击,而不是连续两天在收盘竞拍里重复提交统一规格的大宗 MOC 订单。那些反复出现的 250K 成交块,更像是机构提前计划好的执行策略,而非情绪性回补。

The market’s central debate remains: are these transactions reflecting institutional accumulation, or forced short covering? Short covering is theoretically plausible — as a heavily shorted, high-volatility stock continues pressing toward all-time highs, the pressure of holding short positions overnight escalates rapidly. However, a closer look at the order flow structure suggests this may not be typical short covering behavior. Short sellers generally cover gradually intraday to minimize market impact, rather than submitting repeated uniform-sized MOC block orders across two consecutive closing auctions. The recurring 250K blocks look more like pre-planned institutional execution strategy than reactive short covering.

但市场真正尚未完全定价的,并不是这几天的交易流,而是 AST SpaceMobile 本身正在试图构建的东西。很多人仍然将其理解为一家”卫星公司”,但它真正的目标是把卫星直接变成太空中的手机信号塔——让普通手机在没有地面基站的地方,也能直接获得连接能力,无需特殊天线,无需额外硬件,甚至无需更换 SIM 卡。

But what the market has not yet fully priced in is not the recent order flow — it is what AST SpaceMobile is actually attempting to build. Many still frame it as a “satellite company,” but its true ambition is to turn satellites into mobile signal towers in space, enabling ordinary smartphones to connect directly without ground infrastructure, no special antennas, no additional hardware, and no SIM card changes required.

这也是为什么它的逻辑与传统卫星通信完全不同。$ASTS 并不想像 Starlink 那样向消费者销售终端,而更像是在全球移动通信网络之上叠加一层”来自天空的覆盖层”。运营商继续拥有用户关系、套餐与生态,AST 提供的是覆盖能力本身。当地面基站失效、信号覆盖不到,或根本不值得建设的地方,卫星网络直接接管连接。

This is precisely why its business logic differs fundamentally from traditional satellite communications. $ASTS does not aim to sell terminals to consumers the way Starlink does. Instead, it is layering a “coverage from the sky” network on top of existing global mobile infrastructure. Carriers retain their customer relationships, plans, and ecosystems — AST provides the coverage layer itself. When terrestrial base stations fail, fall short, or simply are not economically viable to build, the satellite network steps in.

问题在于,市场目前很难为这种商业模式估值。它既不像传统电信公司,也不像普通太空企业,更像是在重新定义未来移动网络的边界。过去几十年,全球移动通信的核心逻辑始终是谁拥有更多地面基站;而 AST 想做的,是让天空本身成为网络的一部分。当然,这条路的执行风险仍然极高——卫星部署、资本开支、频谱协调、运营商合作进度、网络稳定性,以及最终能否形成规模化收入,都将决定它究竟会成为下一代通信基础设施,还是又一个被市场过度想象的太空叙事。

The challenge is that the market currently struggles to value this kind of business model. It resembles neither a traditional telecom nor an ordinary space company — it is closer to something redefining the boundaries of future mobile networks. For decades, the central logic of global mobile communications has been who owns more ground-based towers. AST’s proposition is to make the sky itself part of the network. That said, execution risk remains extremely high — satellite deployment, capital expenditure, spectrum coordination, carrier partnership timelines, network reliability, and whether scalable revenue can ultimately be achieved will all determine whether this becomes next-generation communications infrastructure or another space narrative the market has over-imagined.

市场上真正开始分化的,并不是短期股价的走向,而是两种完全不同的世界观。一种认为 $ASTS 只是一家尚未盈利、高烧钱、高风险的卫星概念股;另一种则开始将其视为未来全球移动网络的一层基础设施。如果最终是后者成立,那市场现在讨论的,可能根本不是短期估值,而是未来十年通信网络结构会否被彻底重写。下一份 FINRA 空头持仓数据,或许将为市场提供更清晰的答案:最近这些异常庞大的收盘竞拍订单,到底是谁在持续买入。

The real divergence forming in the market is not about near-term price direction — it is a clash of two fundamentally different worldviews. One camp sees $ASTS as an unprofitable, cash-burning, high-risk satellite concept. The other is beginning to view it as a foundational layer of tomorrow’s global mobile network. If the latter proves correct, what the market is debating today may not be short-term valuation at all, but whether the architecture of global communications will be rewritten over the next decade. The next FINRA short interest data release may offer a clearer answer: who exactly has been the persistent buyer behind these unusually large closing auction orders.

随着多项关键催化剂陆续兑现,团队对 $ASTS 的后市部署作出最新评估。具体结论详见以下付费内容。

As multiple key catalysts continue to materialise, the team has completed a fresh assessment of the forward strategy for $ASTS. Full conclusions are available in the paid content below.